Shepherd Outsourcing opened its doors in 2021, and has been providing great services to the ARM industry ever since.

About

Address

©2024 by Shepherd Outsourcing.

.png)

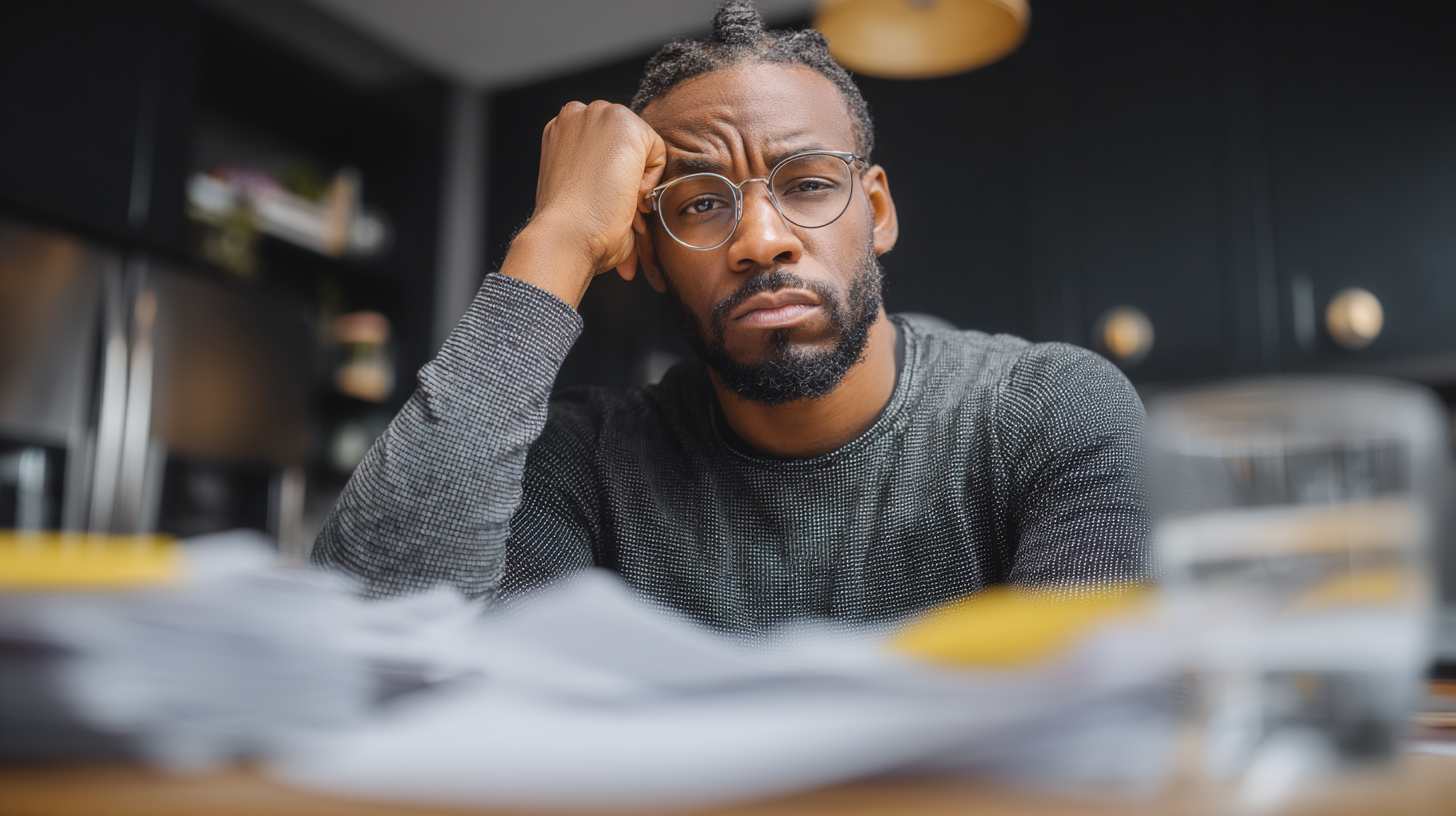

Debt can feel like a heavy weight, be it from medical bills or growing business expenses. In fact, reports show that around 30% of Americans say too much debt is a major barrier to reaching their financial goals, showing just how common this struggle is.

Managing multiple payments, dealing with creditors, and watching debt pile up can overwhelm anyone. But finding the right debt relief option can change that, giving you a clear path to financial recovery.

In this blog, you’ll explore the most common debt relief solutions, how they work, and how you can pick the one that fits your situation to control your finances.

Debt relief helps individuals get their debt under control by reducing or restructuring it, making it easier to manage. People often turn to debt relief when balances become overwhelming, especially with high interest rates and multiple creditors demanding payment at once.

By choosing debt relief, you may be able to lower what you owe, free up monthly cash flow, and take steady steps toward getting back on track financially.

Once you understand debt relief, it becomes easier to see the common options for managing and reducing debt.

When debt becomes overwhelming, finding the right solution can be stressful and confusing. The good news is that there are several debt relief options that can help lower what you owe and put you back in control of your finances.

Here’s a simple breakdown of the most common debt relief options that may work for your situation:

Debt settlement is a common option for individuals who realistically cannot repay their debt in full. This approach allows yoy to settle the debt for less than the total amount owed.

Here's how it works:

Many people choose to work with firms like Shepherd Outsourcing, which negotiate with creditors on their behalf. They provide structured support to organize settlements and manage payments effectively. This professional guidance can make the debt settlement process smoother and less stressful.

Suggested Read: How to Negotiate a Debt Settlement with Collectors

Debt consolidation combines multiple high-interest debts into one loan with a lower interest rate. This makes debt easier to manage by replacing several payments with a single monthly payment.

Here's how it works:

A Debt Management Plan is a structured repayment program handled by a certified credit counseling agency. You make one monthly payment to the agency, which then distributes it to your creditors.

Here's how it works:

If debt becomes unmanageable, bankruptcy may offer relief by either clearing unsecured debt through Chapter 7 or restructuring debt through Chapter 13.

Here's how it works:

Knowing the common debt relief options clarifies which types of debt typically qualify for relief.

Debt relief can be a helpful option if your financial obligations feel overwhelming. Knowing which types of debt qualify for relief makes it easier to take that first step toward getting your finances back under control.

Medical debt can build quickly, especially without insurance or with high out-of-pocket costs. Debt relief, through settlement or consolidation, can reduce these bills and make them easier to manage without sacrificing care.

Personal loans often come with fixed payments and interest that strain your budget. Debt relief can help settle the loan for less or combine payments into a single, manageable amount.

Small business owners may struggle with unsecured loans or lines of credit. Debt relief can reduce debt, improve cash flow, and lower risks to personal assets.

There are several other types of debt that also qualify for debt relief:

Once you understand which debts qualify for relief, it makes it easier to see how debt relief actually works in practice.

Also Read: Effective Debt Management Strategies and Tips

Debt relief provides a clear, organized way to tackle overwhelming financial obligations. It helps reduce or restructure debt, making what you owe easier to manage. Here’s how it typically works:

The process starts with reviewing your debts, income, expenses, and financial goals. Understanding what you owe and what you can afford allows a debt relief provider to create a plan tailored to your situation.

Once your plan is set, your debt relief provider works directly with your creditors on your behalf. The goal is to reduce the total amount you owe, lower interest rates, or adjust repayment terms.

Working with professionals like Shepherd Outsourcing makes this process easier to manage. They coordinate with creditors, organize payments, and provide structured guidance to help you stay in control of your finances.

Once negotiations are complete, a payment plan is set up, often combining multiple payments into a single payment. Whether via lump-sum or monthly installments, the plan is designed to fit your budget and steadily pay down debt.

Debt relief includes long-term support. Providers may offer check-ins, updates, and budgeting and money management advice to help you avoid future debt and build healthier financial habits.

Knowing how debt relief works also brings attention to the risks you should consider before deciding if it’s the right option for you.

Must Read: Top 6 Debt Settlement Companies: How They Work & How to Choose One

Debt relief can feel like a lifeline if you’re dealing with overwhelming debt, but it’s important to understand the risks before moving forward. Here are the key risks you should know about:

Debt settlement can lower your credit score because accounts show as “settled for less.” Consolidation or management plans may have smaller effects, but changes in payment terms can still impact credit.

Debt relief often comes with fees, such as service charges, interest, or administrative costs. Without careful review, these fees can add up and increase financial strain.

Some companies make unrealistic promises, charge high fees upfront, or mislead consumers. Always research reviews, verify accreditations, and confirm credibility before enrolling.

In some cases, forgiven debt may be treated as taxable income. For example, if $10,000 is forgiven, the IRS may count it as income, increasing your tax bill if you're unprepared.

Some programs require pausing payments while saving for settlements. Missed payments can hurt credit, incur fees, or trigger legal action, such as wage garnishment.

If a creditor rejects a settlement, you may still owe the full balance. Some creditors may pursue legal action, including liens or wage garnishment. Not all settlements succeed.

Secured debts, like mortgages or auto loans, don’t qualify for debt relief. Understanding these limits upfront is essential.

Once you’re aware of the risks involved, it's easier to explore alternative options that might better suit your financial situation.

While debt relief works well for many individuals and businesses dealing with debt, it isn’t the only option to consider. Depending on your financial situation, other approaches may help you manage your debt more effectively.

Below are key alternatives to debt relief worth considering.

Credit counseling involves working with a certified counselor to create a plan to manage your debt. It focuses on budgeting, controlling spending, and avoiding future debt. This works well if you want guidance and education instead of direct debt reduction.

If your income isn’t enough to keep up with debt, focusing on earning more is another option. This may include taking a side job, asking for a raise, or selling unused items. While it takes effort, it allows steady progress without harming your credit.

Borrowing from family or friends can help pay off debt, but clear repayment terms are essential. Treat the agreement seriously and ensure both sides are comfortable from the start.

Exploring these alternatives also helps you decide whether debt relief is truly the right choice for your situation.

Debt relief offers a fresh start, but it isn’t the right fit for everyone. It works best for people facing overwhelming debt who need a clear, structured way to regain control. Here’s when debt relief might make sense for you:

Shepherd Outsourcing helps make debt relief more manageable by providing structure, guidance, and coordination throughout the settlement process. They focus on negotiating with creditors, organizing payments, and ensuring agreements are executed properly.

Here’s what their support includes:

By coordinating negotiations, providing structured plans, and offering ongoing guidance, Shepherd Outsourcing helps make debt relief clearer, more organized, and easier to manage.

Debt relief can help you take back control of your finances, but it’s important to look at all your options before deciding what’s right for you. Take the time to list your debts, confirm your balances with creditors, and determine which payment plan would be most manageable for you.

Working with professionals like Shepherd Outsourcing can help turn your debt information into a structured, actionable plan. Their team communicates directly with creditors, negotiates repayment or settlement terms, and offers guidance to make the process easier while staying within legal requirements.

Connect with us today to explore how a supported debt settlement approach can help you take the first step toward managing your debts and regaining financial control.

A1. Some types of debt usually do not qualify for debt relief, including:

A2. The timeline depends on the method. Debt settlement can take several months to a few years, while consolidation or management plans often take several years. You typically see results as your balances decrease and you make regular payments.

A3. Federal student loans generally don’t qualify for debt relief, as they have separate repayment and forgiveness programs. Some private loans may qualify, so check with your lender or a financial advisor.

Q4. Can debt relief be used more than once?

A4. Yes, but repeated use may indicate underlying financial issues. Long-term improvement often requires better budgeting, financial education, or changes in spending habits.

A5. The IRS may treat forgiven debt as taxable income. That means you could owe more at tax time, so it’s a good idea to talk with a tax professional and understand the impact before moving forward.

©2024 by Shepherd Outsourcing.