Shepherd Outsourcing opened its doors in 2021, and has been providing great services to the ARM industry ever since.

About

Address

©2024 by Shepherd Outsourcing.

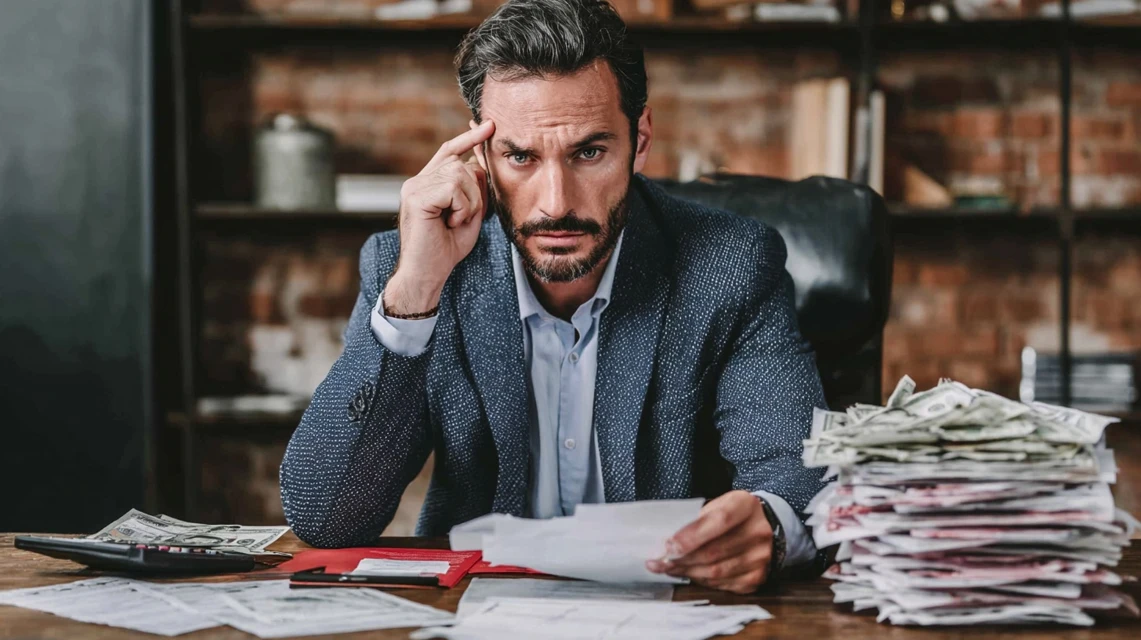

Did you know that total U.S. household debt reached approximately $18.8 trillion in late 2025? It continues to grow as people and businesses borrow more to cover everyday expenses and overdue obligations. Managing multiple debts under these conditions can quickly feel overwhelming.

Missed payments, rising interest, and constant creditor calls add stress and uncertainty for both individuals and businesses, making it hard to plan or regain control. This often leads to a critical question: “Is debt settlement worth it?” When done correctly, debt settlement offers a structured way to reduce debt obligations while creating a clear path toward financial stability.

In this blog, you’ll learn what debt settlement is, how it works, its benefits and risks, and the steps you can take to make informed decisions about your financial future.

Debt settlement is a structured process in which a debtor negotiates with creditors to pay less than the total amount owed. For individuals, it reduces financial stress and simplifies repayments. For businesses and creditors, it helps recover outstanding balances efficiently without legal complications.

Debt settlement helps both debtors and creditors regain control of their finances, reduce risk, and resolve outstanding debts in a clear, legally compliant manner. Understanding the process step by step shows exactly how it leads to real financial relief. Let’s break down the process step by step.

Debt settlement follows a structured process designed to help you reduce your debt efficiently while maintaining financial stability. Each step provides clear actions and practical strategies to help you resolve outstanding obligations without unnecessary stress.

Start by taking a close look at all your outstanding debts, interest rates, and creditor information, including overdue invoices or unpaid client balances for businesses.

Once you understand your debts, the next step is to negotiate directly with your creditors.

Reach out to your creditors to propose a reduced payoff. Successful negotiation can lower your balances and help you avoid costly legal action.

Once a negotiation succeeds, your creditors will provide a written settlement agreement outlining the exact payment amount and timeline. Many agreements allow for installments, offering flexibility.

Follow the settlement plan and make the agreed-upon payments. Completing payments on schedule ensures the debt is fully resolved.

Debt settlement often includes advice on improving cash flow, managing expenses, and preventing future debt. For businesses, this may involve strategies to strengthen receivables and reduce overdue client balances.

Following these steps can be challenging, but professional guidance makes the process easier. Debt settlement partners, such as Shepherd Outsourcing Collections, guide you through every stage, from negotiating with creditors to creating customized repayment plans. This approach ensures clear, efficient, and fully compliant results while helping you reduce your total debt and regain financial control.

Also Read: Debt Settlement vs Bankruptcy: What’s Right for You?

Beyond simply lowering your debt, debt settlement provides benefits that many debtors often overlook at first. Let’s explore how these advantages can improve your financial stability and simplify repayment.

Debt settlement can offer advantages beyond immediate financial relief, including long-term stability, simpler payments, and professional support to help manage your obligations effectively.

Taken together, these advantages make debt settlement a strategic way to regain control, simplify payments, and protect your financial stability.

If you need guidance on negotiating with creditors or structuring manageable repayments, Shepherd Outsourcing Collections offers compliant and personalized settlement plans that reduce financial pressure without involving the court.

While settling debts can be a smart move, being aware of potential pitfalls helps you make informed decisions and avoid surprises. Let’s explore the key risks you should consider before committing to a debt settlement plan.

Debt settlement can provide relief, but it’s important to understand the potential risks before making decisions. Being aware of these challenges helps you prepare, reduce surprises, and maintain financial stability.

Settling a debt for less than the full amount can affect your credit history and how lenders view your financial reliability.

Professional debt settlement services charge for their expertise, which can affect overall savings from debt settlement.

Some debts cannot be negotiated through settlement, which may limit your options or prolong financial obligations.

Forgiven debt can sometimes be considered taxable income, which could create additional financial responsibilities.

Ensuring that agreements comply with legal requirements is essential to protect yourself and avoid disputes.

Also Read: Effective Commercial Debt Recovery Solutions: Strategies to Improve Cash Flow and Minimize Risk

To determine if this approach works for you, consider some key factors that influence whether debt settlement is the right choice.

Determining whether debt settlement is the right choice requires a careful review of your financial situation and long-term goals. Making an informed decision helps you answer the key question: Is debt settlement worth it? Consider these critical factors:

Debt settlement works best for high unsecured debts that are difficult to manage with regular payments.

Your ability to meet lump-sum or installment payments is essential for a successful settlement.

Explore other repayment strategies before committing to settlement:

Debt settlement should support your broader financial strategy, not just provide short-term relief.

By reviewing these factors in detail, you can determine whether debt settlement is a practical and effective solution for regaining control of your finances.

To understand your options more clearly, let’s compare debt settlement with other common debt relief strategies.

Debt settlement often provides a middle-ground solution: lower debt without the extreme consequences of bankruptcy, backed by professional support. So, when is debt settlement truly worth considering? Let’s explore some real scenarios.

Debt settlement can be a practical solution when your financial obligations become unmanageable. It works best in situations where standard repayment strategies aren’t enough, and professional negotiation can make a real difference.

You might consider debt settlement if:

Working with a professional partner ensures your debt reduction strategy is tailored to your situation, legally compliant, and designed to protect your financial interests while lowering your total debt.

Next, let’s explore how Shepherd Outsourcing Collections can help you achieve these results.

At Shepherd Outsourcing Collections, we help individuals and businesses across the U.S. regain financial stability through structured debt settlement programs. Our approach focuses on reducing your total debt while ensuring compliance and long-term financial security. Our services include:

We aim to resolve your debt challenges efficiently, without the lasting impact of bankruptcy. Whether you are an individual or a business, our team handles your settlement plan professionally, securely, and with full transparency.

Deciding whether debt settlement is right for you isn’t about taking shortcuts; it’s about choosing a practical path to regain financial stability. The right approach depends on your income, financial goals, and long-term plans. Acting early, with professional guidance, can help you reduce stress, minimize long-term impacts, and rebuild your financial foundation with confidence.

If you’re struggling with debt or facing pressure from creditors, Shepherd Outsourcing Collections can help. Our team provides professional, compliant, and tailored debt resolution services designed to simplify the process and protect your interests.

Take control of your finances today. Contact us to learn which debt solution works best for you.

Debt settlement may initially lower your credit score because creditors report partial payments. However, responsibly completing settlements, making timely payments on other accounts, and managing future debts can gradually rebuild your credit and demonstrate improved financial responsibility to lenders.

The timeline depends on your total debt, creditor responsiveness, and negotiation complexity. Most debt settlements take between 6 and 24 months. Smaller balances or fewer creditors may settle faster, while larger or more complex accounts require careful planning and scheduled payments over time.

Not every debt can be settled. Typically, unsecured debts such as personal loans or medical bills are eligible. Secured debts, including mortgages, auto loans, and taxes, usually cannot be negotiated. Reviewing debt eligibility upfront helps set realistic expectations and avoids delays in the settlement process.

Professional debt settlement partners handle creditor communications to minimize stress. While you may still receive notices or updates, direct contact is largely reduced. This ensures negotiations remain organized, compliant, and focused on achieving reduced balances without unnecessary conflict.

Settling debts can reduce the risk of creditor lawsuits, but it does not guarantee full legal protection. Prompt negotiation, timely payments, and professional guidance reduce exposure, ensure compliance with laws, and provide documented agreements that may help defend against potential legal challenges

©2024 by Shepherd Outsourcing.